Speaking of pandemics and awesome news, I saw this last week and thought it worth passing along…

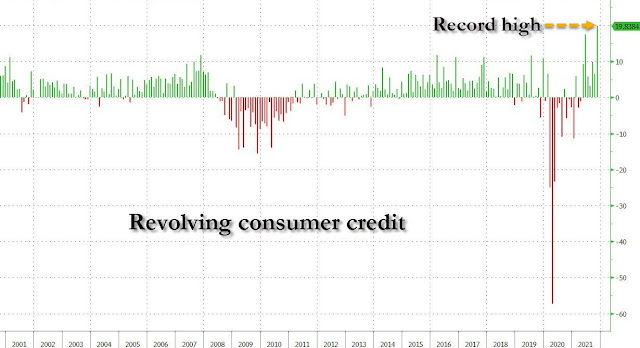

While it is traditionally viewed as a B-grade indicator, the November consumer credit report from the Federal Reserve was an absolute stunner and confirmed what we have been saying for month: any excess savings accumulated by the US middle class are long gone, and in their place Americans have unleashed a credit-card fueled spending spree.

Here are the shocking numbers: in November, consumer credit exploded by a whopping $40 billion, double the expected $20 billion print, more than double the $16 billion October number, and the highest on record!

… the real stunner was revolving, or credit card debt, which more than tripled in November, soaring to $19.8 billion from $6.6 billion in October, by far the highest such print on record.

RTWT. This is the critical chart…..

“revolving debt” is a fancy term meaning lines of credit, most commonly credit cards and to a lesser extent things like home equity lines of credit, or HELOCs in the banking biz. This is in contrast to traditional loans like car loans and mortgages that generally are a fixed amount borrowed and paid down over time, while with revolving debt the principal balance is always fluctuating.

The economy is on life support and the only thing keeping it going is consumer spending driven by unsecured credit card debt, plus government spending using “money” whipped up out of thin air.

This explains why even though apparently no one is working and inflation is at a 40 year high, people seem to keep buying stuff. There are almost as many Amazon, UPS and FedEx trucks running the roads now as there were right before Christmas so people haven’t stopped spending.

The usual problem with revolving debt is that people keep adding to it and not paying it down. A lot of people are going to be surprised when they file their taxes and realize they got a bunch of their fully refundable child tax credit in installment payments last year as they are probably relying on their “tax return” to pay off their credit cards.

Lots of Americans have racked up lots of unsecured debt and the more they pile up, the larger the minimum payments they owe each month. The end result of this is predictable, more people defaulting on credit card debt and more personal bankruptcies.

Unsecured debt fueled consumer spending is one of the key components of the house of cards that we call the American economy. All of those stores, online retailers and restaurants that keep popping up are relying on an endless and, this is important, ever-increasing firehose of credit card debt to keep selling their crappy wares. One reason Big Business loves unlimited mass immigration is cheap labor but the flipside is that the same cheap laborers are also new consumers of crap made overseas.

Much of our economic system in 2022 is based on consumers buying goods made somewhere else with “money” that doesn’t exist. It is a perfect storm of fragility and it won’t take much of a shock to make it come apart.

What concerns me most of all about the surge in debt is a fear that Droopy Drawers Biden or his leftist proxies will push through some sort of forgiveness plan for outstanding consumer debt, just as they wish to cancel student loan debt.

We received not one thin dime of any of the "stimulus" checks handed out like Tic Tac mints last year. And we carry precisely zero revolving debt, since we are sufficiently astute to realize that 14.99% interest (or more) on prior purchases, while earning 0.05% interest on passbook savings, is not consistent with positive wealth management. Forgiving some lout's credit card debt for financing an 85" TV at usurious rates would be de facto punishment to those of us who live without our means.

Would this administration be that stupid? Oh, yes, this administration would be that stupid.

TBC

I know someone who is taking a Calculated Risk of running up "Credit" to buy Supplies for the Zombie Apocalypse. Property and Vehicles are "Paid for", making them Harder to "Take" in a Legal sense. Carefully Increasing the balances on numerous CC's by making Minimum Payments until his Budget reaches a certain, calculated Limit for that, and then the Plan is, once the "Collapse" Hits, Max Out all the Cards and Throw them Away.

That is definitely on the wish list for the extreme left, some sort of mass debt "jubilee" that would forgive basically all debt via government bailout.

I can see the sense of that strategy, even in bankruptcy you can shield your house and vehicle debt in most cases. Of course I am not recommending that strategy but I can see the point.

I took the same calculated risk in '20/'21. I didn't have a single credit card from the late 1980's until 2019 and carried no debt. When "the Plague" hit, I looked at my current level of preps and went a little off the rails and filled all the gaps I could find. Now, I'm much better prepped and have a level of debt that I can clear within a year if the wheels don't come off between now and then. And if everything goes to crap, my debt will be the least of my worries.

I am always looking for ways to convert my fiat currency into durable goods. To that end, my credit cards ran up their highest monthly balances in a long time. BUT!!!! I pay them off religiously, every month, and pay not one thin dime in interest. Do my charges show in this data? No idea.

We worked long and hard to retire debt free, and I am obsessive to the point of paranoia to stay that way. The credit cards I use are "1% cash back" deals and that adds up over time. Also no service charges or interest paid AT ALL. My preps are not only to weather the 'pockyclips, they're also a hedge against inflation on every item I buy now.

The old man that got me started in prepping cashed in a retirement fund and bought a shit-ton of silver in 2011 when it was $37 an ounce. He passed away in the mid-20teens of cancer when silver was about $14 an ounce and his wife was forced to sell to pay bills. Instead of being the hero of the apocalypse, to his family he was the dummy that sold what would have been worth hundreds of thousands. Sometimes that "calculated risk" is a bitch.

Not good. Hope they're buying staple foods instead of Netflix.

You know better than that but I appreciate your optimism.

We pay ours off every month as well and use cash back cards, over the last couple of years a couple of additions to my safe/ammo stash were paid for with the reward money.