From 2005 to 2008 I worked as a bank manager for two banks, one was a giant international bank and the other was a Midwestern super-regional bank. I didn’t really like the industry at all, although I did like aspects of banking, especially helping customers. But that was completely overshadowed by the endless pressure to sell, sell, sell. We had annual goals broken down to weekly goals which became daily goals. Open more checking accounts, close more loans, set people up with credit cards. You could have a super busy day, helping lots of customers with problems and building great relationships but if you didn’t open any new checking accounts you could expect a phone call. The ethical lines got pretty blurry at times which was a major factor in me leaving retail banking. A few years ago, Wells Fargo got into a bunch of trouble for fraudulently opening millions of checking accounts and credit cards without customer authorization. When I heard of this, my initial reaction was “Yep” and a little surprise that a) it took that long to come out and b) that more banks haven’t been busted. That’s all I say about that. Wells has since modified their incentive program to eliminate the high pressure product goals. My point is that banking is highly competitive and bankers are always on the prowl for new accounts, new loans and new investments.

Well over the last few days I have gotten into a twitter scuffle (several actually) based on a post from Kyle Howard. Mr. Howard styles himself a preacher and Bible teacher, but also “Biblical Counselor (including race based trauma)”. So when he made a claim that Asians are not very good “allies” for blacks in their struggle and that Asians have been “granted” social and economic “privilege” and I push back, the responses were predictable….

|

| Me pushing the “tweet” button and girding my loins for battle |

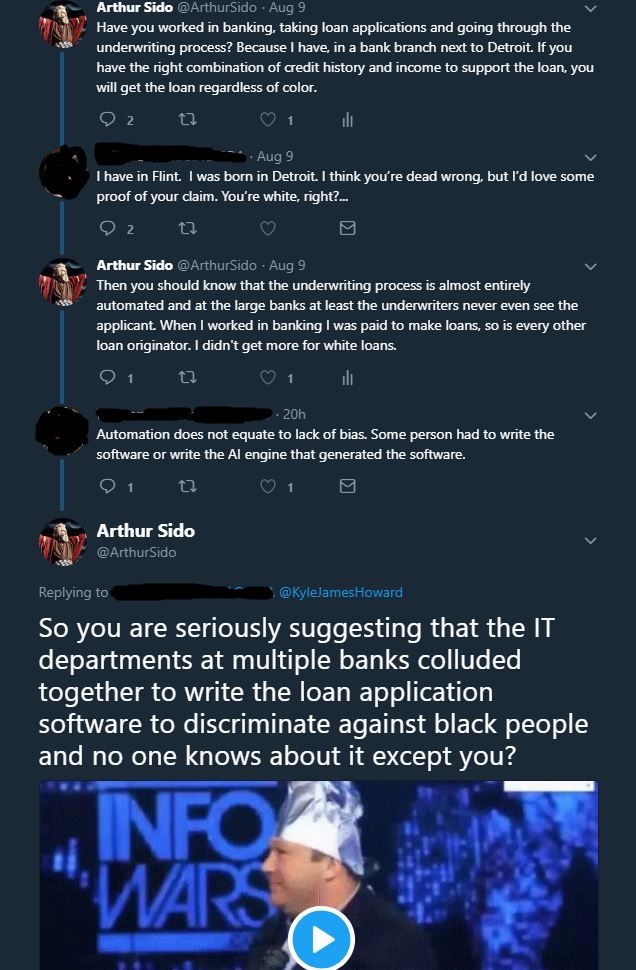

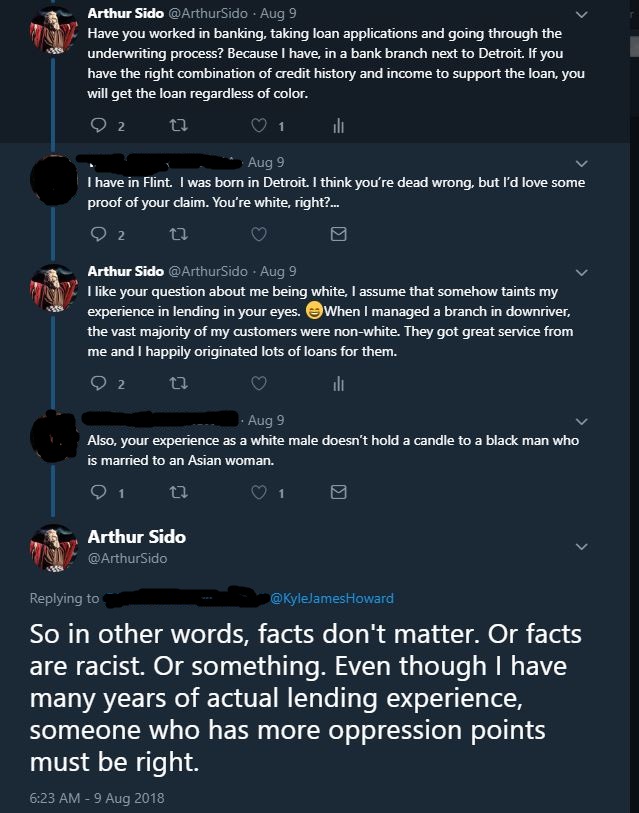

The thread devolved into a discussion of alleged discrimination against black mortgage applicants. Yeah, I know. Here is the thread in a couple of parts, I added the one where a lady said that my experience in lending is negated by being white. Although these are public tweets and you can easily find the names, I still marked out the names and avatars to protect the ignorant innocent.

I get it. Most people don’t really understand how banks make money. It is not that complicated but they just have never been exposed to it. Banks make money in a lot of ways, like investments which are very lucrative and fees on accounts, loans and credit cards plus small amounts on debit card transactions, etc. But the real bread and butter of most banks is lending in a fractional-reserve system. This is basically how it works. People deposit money in bank accounts like checking and savings. These funds make up the deposit balance of a bank. The bank pays depositors a small amount of interest on savings and some checking accounts. On the other side, banks lend borrowers money to buy homes and cars. They charge the borrowers interest on the money lent. The difference between the interest paid on deposits and the interest charged, called the net interest spread or just spread, is where banks make their money. This is why interest rates paid on CDs and savings are so low and have been for years, because banks are charging relatively low rates on loans. I am not sure what the current rates are but when I left banking and up until recently, the interest rate on a savings accounts was functionally zero.

Most people think of a bank as a place to deposit money and to write checks from but that is really incidental to the bank, and messing with checks and cash is a hassle that banks would prefer to not deal with. Ideally a bank would get nothing but direct deposits and pay out only electronically. Banks act as an intermediary between depositors and borrowers. Thousands of people deposit money at a bank which creates a pool of money for a borrower to tap into for big purchases like a mortgage. If you didn’t have banks and wanted to borrow $100,000 to buy a house, you would have to convince enough individuals to loan you their excess cash to raise the $100,000. Banks do that for you. There are lots of issues with this system. For example, most people would be surprised to find out how little actual cash there is in a bank. If a significant number of depositors showed up at a local branch and wanted all of their money, the branch would run out of cash in a hurry. In fact we would get in trouble from the higher ups if we had too much money on hand, so it was always a balancing act to make sure you have enough for daily demand, to keep the ATM full, etc. but not too much so branches constantly send money out and get different denominations in.

How do banks make money? Banks make money by making good, solid loans with a reasonable certainty of being repaid. Lending is all about balancing risk. Banks want to make loans but they want those loans to be repaid so they get their principal back plus interest. What they do not want is to foreclose on a house or repossess a car. That is hugely expensive and they usually take a bath on the property. During the financial crisis, a lot of banks essentially stopped foreclosing on delinquent mortgages because they already had too many homes that they have to try to resell, again often for a loss, and in the meantime they have to maintain the property so it doesn’t lose even more value. Banks are lenders, not property managers.

Back to risk. How does a bank gauge risk? This is important because the more risky a loan is, the higher interest rate the bank will charge because they are less certain of being repaid. Someone with great credit and low outstanding debt relative to their income (debt to income ratio) will get a lower interest rate on a loan because they are less risky. Someone with poor credit and a lot of existing debt will be assessed a much higher rate to offset the bank’s risk. How does a bank make this determination for a pool of tens of millions of potential borrowers? In the old days when banking was more local, it was based on relationships. Suzy has been a long time customer of the bank, has a solid job history and has paid back loans before so she is a good risk. Tom is always overdrawn in his checking account, had a car repossessed by the local bank and is often changing jobs so he is a poor risk. This is sort of how some of our local banks around here operate because of our large Amish community. They make better borrowers because the older members of the community will often act as a de facto guarantor of loans for younger Amish. But today that is not realistic because people move around a lot and banks have too many customers to get to know them. Plus basing credit decisions on relationships also creates a lot of subjectivity. So banks use credit scores as their main initial qualifier.

Credit scores are not perfect but they do provide a neutral means to track credit history. If you borrow money and you pay as agreed (which is what your signature on a credit slip means), your credit goes up (influenced as well by lots of other factors like total available credit, credit inquiries, etc.). If you borrow money (credit card, car loan, mortgage, etc.) and you don’t pay as agreed, your credit goes down. Again, not a perfect system but it does provide the most objective measurement of credit history which is, like it or not, the best gauge a lender has of the likelihood you will pay back a loan.

The other side of risk that is less obvious is the risk of being too conservative. Sitting on money you are paying interest on means you are losing profit every day it sits in your virtual vault. It is not just the mitigating of risk of loan default, it is also the risk of not lending enough to make your profit. A bank paying interest to depositors and not getting interest paid on loans goes out of business. So banks want to make good loans. They have to make good loans and they need to keep making loans because people pay off existing loans early or refinance somewhere else or the loan just gets to the end of the term and is paid off naturally. A bank manager with a huge portfolio of solid, profitable loans making money that is not building their loan portfolio with an active pipeline of new loans is going to get phone calls and will lose their job pretty quickly.

Like I said, banking is a highly competitive, very stressful and cutthroat industry. Everyone I knew was too busy trying to make their goals each week to waste a good loan opportunity just to screw over a black person. If a customer that happened to be black, Hispanic, Muslim whatever, came into my branch and asked to apply for a loan, you can bet I took their application eagerly. First of all, by law I was required to. Second, I needed to get as many loans into the pipeline as I could. A lot of people of every race came in to apply for loans and a lot of them I was pretty sure were not going to be approved but I took every application and treated everyone fairly because it was the right thing to do. Of course I also learned early on in banking that looks can be deceiving, often the old guy in bib overalls with the “aw shucks” demeanor had a ton of money and the people with the fancy car and expensive clothing lived paycheck to paycheck.

So one the ones side you have enormous pressure to only make good loans and on the other hand you have just as much pressure to make lots of loans. Most of the pressure on the first is taken away from lenders. The people you see in branches or mortgage offices are just taking the app and collecting the documentation. They don’t make the decisions. An underwriter sitting in some prison office complex somewhere makes the decisions, mostly via automation.

As I said to someone I respect on Facebook; what possible reason would an underwriter sitting in some cubicle farm with a never ending queue of loan apps have to pick out otherwise solid applications because of the last name? That just stretches the bounds of credulity. If you have decent credit, a reasonable debt to income ratio, a steady job history and the value of the collateral doesn’t exceed the amount of the loan, all things being equal you will be approved. If you don’t, you either won’t be approved or you might be approved for a loan with a much higher interest rate and it has been my experience that people who were shaky loan candidates that managed to get approved anyway were very quickly over their heads. Like insurance companies that rely on being right about life expectancy to make money on life insurance, so too do banks rely on being right about loans to make their profits.

So where does this idea of banks discriminating against blacks come from? Certainly in the past this was a huge issue. That was the reason for the Community Reinvestment Act passed in 1977. This bill is not without it’s critics. As Ron Paul wrote: “Laws passed by Congress such as the Community Reinvestment Act required banks to make loans to previously underserved segments of their communities, thus forcing banks to lend to people who normally would be rejected as bad credit risks.”.

The notion that there is still widespread, systemic discrimination comes from stories like this in the Detroit News: Detroit-area blacks twice as likely to be denied home loans. That certainly sounds ominous, right? Detroit is the “blackest” major city in the country, as recently as 2010 it was over 82% black while the white population plummets and the Hispanic population percentage increases rapidly. Detroit also has a very low median family income and around a third of the population lives in poverty. The article linked above clearly tries to show that this is do to discrimination but buried in the story are some important facts.

Lenders and their trade organizations do not dispute the fact that they turn away people of color at rates far greater than whites. They maintain that the disparity can be explained by two factors that the industry has fought to keep hidden: the prospective borrowers’ credit history and overall debt-to-income ratio. They singled out the three-digit credit score — which banks use to determine whether a borrower is likely to repay a loan — as especially important in lending decisions.

“While quite informative regarding the state of the lending market,” the records analyzed by Reveal do “not include sufficient data to make a determination regarding fair lending,” the Mortgage Bankers Association’s chief economist, Mike Fratantoni, said in a statement.

The American Bankers Association said the lack of federal enforcement proves discrimination is not rampant, and individual lenders told Reveal that they had hired outside auditing firms, which found they treated loan applicants fairly regardless of race.

“We are committed to fair lending and continually review our compliance programs to ensure that all loan applicants are receiving fair treatment,” Boston-based Santander Bank said.

Michigan lenders echoed their national counterparts, saying the mortgage process isn’t discriminatory but instead is driven by data: credit, collateral and income.

“Lending today is so automated,” said Jim Wickham, president of the Michigan Mortgage Lenders Association. “It’s difficult for me as a lender to look at this … data and see discrimination.”

Exactly so. The process is automated, it is heavily regulated and the same story shows that even under the Obama administration only 9 banks nationwide had action taken against them during his 8 years in office, and banks not only use internal auditors but also outside auditing firms to make sure they are in compliance. No bank wants to get dinged under the CRA because that sort of bad publicity will be followed by demagogues like Al Sharpton and Jesse Jackson looking for a handout. It is just too big a risk.

Banks freely admit they turn away blacks at a much higher rate and the reason is two-fold: credit scores and debt-to-income ratios. The credit score is the big one. The first thing the loan application system does is pull your score and right away that is going to either immediately disqualify you or advance you in the process. Likewise debt-to-income, or DTI. Even if you have decent credit and income, if your outstanding debt that you need to service eats up too much of your income, you won’t get approved. This is not a racial issue, this is simply a risk factor. Again, and this cannot be overemphasized, the loan underwriting process is all about managing risk. Will you be likely, based on your income, outstanding debt and your credit history, to pay back money if it is lent to you? Keeping a good credit score is simple: Pay what you owe when you owe it. Show you are responsible with the credit you already have and you are far more likely to get more credit in the future.

A great resource on this is an article by Coleman Hughes writing for Quillette: Black American Culture and the Racial Wealth Gap. He writes:

To make matters worse, spending patterns are just one part of a larger set of financial skills on which blacks lag behind. Researchers at the Federal Reserve Bank of St. Louis followed over 40,000 families from 1989 to 2013, tracking their wealth accumulation and financial decisions. They developed a financial health scale, ranging from 0 to 5, that measured the degree to which families made “routine financial health choices that contribute to wealth accumulation”—e.g., saving any amount of money, paying credit card bills on time, having a low debt-to-income ratio, etc. At 3.12, Asian families scored the highest, followed by whites at 3.11, Hispanics at 2.71, and blacks at 2.63.

What does that mean? It means that in general, ranked by race, when it comes to overall financial management, blacks score far worse on measures like paying credit cards on time, having a low DTI ratio (quite likely related to the prior paragraph in the linked story that looks at luxury good spending by blacks). If you don’t pay your credit cards on time, it really hurts your credit scores especially if you make a habit of it. If you have too much debt relative to your income, same thing. Mess those two factors up and you aren’t getting a mortgage. That isn’t a sign of systemic racism, everything that can be done is done to take human bias out of the process for a number of reasons.

So what should be done or can be done about blacks being denied for mortgages as such high rates? It is almost entirely a matter of changing a culture. Black civic groups, churches, families, need to emphasize the importance of maintaining good credit by paying debts on time and keeping outstanding debt to a reasonable level. Obviously many black families already do this because they have mortgages and are responsible with credit but the denial rate is still very disproportionate. Instilling a culture of responsible credit will also go a long way toward closing the “wealth gap”. Owning a home has long been the key step in gaining wealth and passing that on to future generations. You can’t help your kids or grandkids to buy their own place if you haven’t accumulated wealth of your own. It won’t happen overnight but it has to start somewhere.